Should I Get a Personal Loan?

Consider a personal loan if you’re consolidating debt or need to fund a large expense like a home remodel.

Personal loans can be used to pay for almost any expense, so it may be hard to tell when getting one is a good idea and when to consider other options.

In some cases, a personal loan can help you meet a financial goal, such as consolidating high-interest debt or financing a home improvement project that increases your home’s value. But it may not be the best option in an emergency or to pay for a discretionary expense like a vacation or wedding.

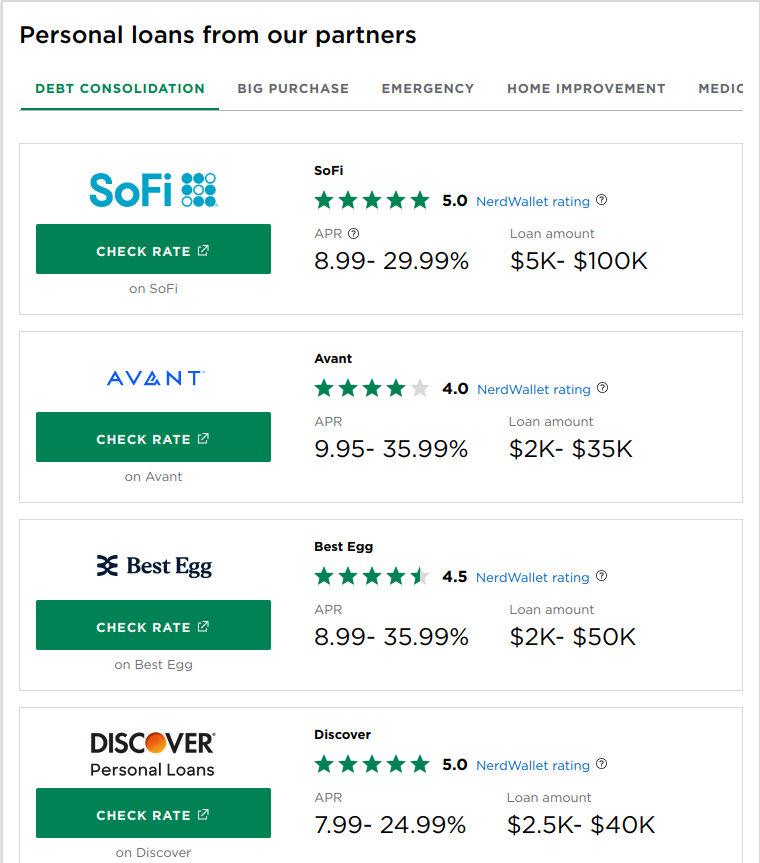

These loans have amounts from $1,000 to $100,000, rates from 6% to 36% and repayment terms from two to seven years. Lenders use your creditworthiness and financial information to determine your personal loan offer. They can be a good way to borrow money if you get a low interest rate and can manage the monthly payments.

Here’s when a personal loan can be a smart financial choice and when to consider alternatives.

When is a personal loan a good idea?

A personal loan can be a good idea when:

- You need the funds fast.

- It is the financing option with the lowest rate.

- You can comfortably afford the monthly payments for the loan term.

Here are common reasons to take out a personal loan:

Debt consolidation

You can use a personal loan to consolidate credit cards and other high-interest debt into a single monthly payment. A debt consolidation loan is typically only a good idea if it has a lower interest rate than your existing debt, allowing you to save money and pay it off faster.

» MORE: Calculate your savings with a debt consolidation calculator

Home improvement

Getting a personal home improvement loan can be an especially smart financial choice if the project adds value to your home. Compare personal loans and other home improvement financing options to get the lowest rate and repayment terms that fit your plans.

» COMPARE: Best personal loans

When does a personal loan not make sense?

A personal loan isn’t a good solution if:

- You have time to grow your savings and can cover your expense in cash.

- You can get a lower rate elsewhere.

- You can’t afford the monthly payments for the loan term.

Here are situations when a personal loan may not make sense:

Discretionary spending

Personal loans are an expensive financing option for discretionary expenses like a wedding or a vacation. Plus, if you use one for this type of purchase, you could be paying for a short-term expense like a vacation for years to come. Instead, consider building up your savings to pay for big-ticket items and avoid finance charges altogether.

Medical costs

Because personal loans can have high interest rates, consider other, more affordable ways to pay your medical bills first. These can include setting up a payment plan with your doctor or hiring a medical bill advocate. Be sure to vet the alternatives carefully to avoid unexpected charges.

Emergency expenses

Personal loans can be cheaper and less risky than payday loans in times of emergency, but they may still have high interest rates, especially for borrowers with poor credit (scores below 630). If you already have an emergency fund, an urgent car or home repair is a good case for using it. If not, consider reaching out to a local financial assistance program or a family member for help.

How to get a personal loan

If you believe a personal loan is the right choice for you, here’s how to get one.

1. Check your credit score. Getting a personal loan starts with checking your credit score against lenders’ borrowing requirements to determine which lenders you may qualify with. Review your credit report and fix any issues that may be hampering your score.

2. Pre-qualify. Pre-qualify to compare potential rates and terms from online lenders, banks and credit unions. Pre-qualifying requires a soft credit check, which won’t impact your score.

3. Compare financing options. Consider other borrowing options that may be available to you, such as a zero-interest credit card — if you can pay off the balance in less than two years. Securing a loan with collateral or adding a co-signer are two ways to potentially lower the interest rate on a personal loan. If rates are similar, check to see if there are any fees or if the lender offers special features, like fast funding or flexible payment dates.

4. Submit your application. If you decide to move forward, gather the required documents so you are ready to formally apply for the loan. This typically requires a hard credit check, which temporarily lowers your credit score by a few points. Applicants with high credit scores, strong income and low debt usually receive the lowest rates.

» MORE: How to get a personal loan